Once again I step into my alter ego role as Mr. Perspective to calm you down about all the Obamacare scare stories that have dominated the news recently, from the disastrous roll out of the HealthCare.gov website to the insurance company cancellation letters.

Let's start with this piece from Nancy Metcalf at Consumer Reports, who investigated the case of Diane Barrette, the Florida woman who made headlines on CBS News and FOX News after she got a letter from Blue Cross Blue Shield canceling her $54/month plan. Unlike the TV journalists, Metcalf actually investigated how good that cheap insurance plan was, and determined that it was essentially useless, the kind of policy that didn't cover Barrette for anything medical that cost more than $50. Metcalf quotes Karen Pollitz, an insurance expert at the Kaiser Family Foundation: "She's paying $650/year to be uninsured."

That type of junk policy is now longer illegal under Obamacare, as it should be. So, while Barrette will have to pay a little more (but still under $200/month), at least she can be secure in the knowledge that when something does go wrong, she'll be covered.

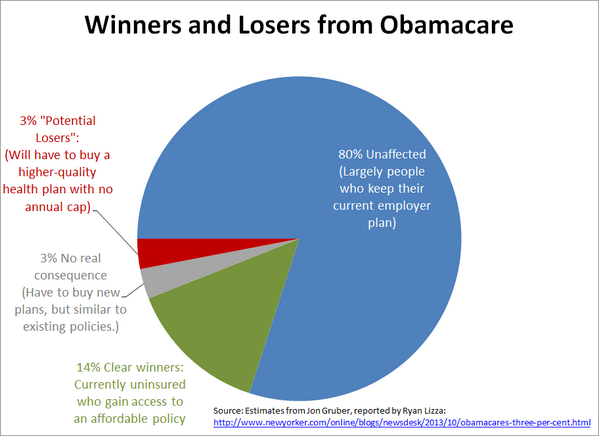

How many Americans will find themselves in Barrette's situation, having to pay more to ensure that they're insured? Check this chart from Justin Wolfers, co-editor of the Brookings Papers on Economic Policy, based on information from reporter Ryan Lizza and MIT economist Jonathan Gruber:

In Lizza's piece, he quotes Gruber, one of the architects of Mitt Romney's health-care plan in Massachusetts, about the winners and losers under Obamacare:

In Lizza's piece, he quotes Gruber, one of the architects of Mitt Romney's health-care plan in Massachusetts, about the winners and losers under Obamacare:

Ninety-seven per cent of Americans are either left alone or are clear winners, while three per cent are arguably losers. “We have to as a society be able to accept that,” he said. “Don’t get me wrong, that’s a shame, but no law in the history of America makes everyone better off.”

And while there were stories last week that only 6 people signed up for health insurance on the first day the exchanges opened, that isn't indicative of anything. Romneycare only enrolled 127 people in its first month, but is now considered a roaring success.

Besides, we are a nation of procrastinators. We don't do our tax returns on January 1. Most of us wait until April to dig out the paperwork and start filling out the forms. Today's November 4th, which means Thanksgiving is three-and-a-half weeks away. Have you started shopping for your turkey and trimmings? No, you'll do that on Wednesday, November 27th.

In the case of Obamacare, the deadline to avoid being penalized for not having health insurance is March 31 -- six full months after the October 1st opening of the federal exchange. What's the last time you did anything six months before it was due? So it's not surprising that a new survey shows that a large number of Americans are aware of the Obamacare exchanges, and plan to enroll at some point, but aren't rushing into anything right now.

Finally, there's this investigation by Dylan Scott, revealing how insurance companies are misleading customers into believing they have to pay much more than they should for decent policies.

Updated at 5:39pm...

Thanks to Eric Monteith for sending me this LA Times story, which debunks yet another Obamacare horror story that's been exploited by news reporters who didn't bother to check the claims of a woman who said she would end up with no insurance because her plan didn't qualify. In fact, she had another one of those junk policies that did her no good, while a new policy under the Obamacare exchange wouldn't cost much more and would offer her real coverage instead.Labels: politics